Burgos, November 17, 2021.- The international economy maintains several uncertainties such as the shortage of materials, the logistical stop, the decrease in production in strategic sectors, and the non-completion of the global Covid19 pandemic. We also have to add the public debt crisis in many european countries and the reconversion of the Welfare State. Meanwhile, China could surpass the United States as the world’s leading power in the coming years.

Undoubtedly, the economic context is complex and needs leadership with a transparent and efficient strategy to get out of this worrying time. One of the escape routes is to think ahead in the short term. In two analyzes by the BBC and FastMarket I have found some keys to help in business planning.

The world economy growing by 5.7% through the end of 2021. We expect growth to slow to 4.6% in 2022. The big unknown in the forecast is China – as a region, it’s the biggest driver of economic growth, accounting for about 30% of global economic growth in 2021. If the Chinese economy slows, the global economy will slow significantly too unless other key regions massively outperform forecasts. The rising cost of living is a hot topic around the globe in the final quarter of 2021. Is inflation a temporary effect of the Covid-19 rebound or something longer-lasting? We think it’s both; it depends on the sector.

Some sectors will see temporary price increases caused by supply chain challenges and other bottlenecks. When operations return to normal, prices will normalize too. But factors such as the cost of energy and the availability of truck drivers will have a longer-term effect on some sectors such as the energy-intensive steel industry and the logistics-dependent retail sector. Sustained high costs will inevitably be passed onto consumers.

The energy transition could also drive up prices in the long term. Carbon taxes and the cost of complying with new regulations will increase the cost of supply, and, again, it is consumers who will pay.

Producer price indices in Europe, the US and China all reflect rising costs in the short and long terms and are all trending high compared with the past 15 years, suggesting the start of a period of sustained high prices.

When inflation crosses the red line in the chart above, it’s often associated with a memorable event such as the energy crisis in the 1970s. Could Covid-19 be the catalyst for unusually high inflation in 2022?

If inflation continues while growth slows and wages stagnate, we may enter a period of stagflation or recession-inflation not seen since the time of the 1970s energy crisis. If central banks intervene on inflation by reducing economic stimulus and perhaps increasing interest rates, this would increase the cost of capital and dampen growth. (The ECB, the Fed and the Bank of Japan are already showing signs of cutting back on Covid-19-era spending.) Similarly, rising interest rates could pose a threat to governments that have accumulated unprecedented Covid-era debts. There’s no quick fix for a stagflation-like scenario.

US economic outlook 2022: not yet the ‘normal’ year many hope for

We expect to see 6.3% growth for the US this year while its economy recovers from Covid-19 – the growth rate in 2020 was 3.4%. Still, growth looks set to slow in 2022 to 4%.

In the US, consumption is roughly 70% of GDP. The US economy is driven by consumption of goods and services, with services making up nearly two-thirds of total consumption. The consumption of services fell during Covid-19 because of lockdowns and other restrictions. It has yet to recover to 2019 levels. Slow recovery in the service sector is dampening growth and represents a downside risk to the US economy.

We also looked at the US labor market, which has a bearing on consumption levels. In Q3 2021, there are around 5.3 million open jobs – a classic good news/bad news metric. While open jobs are a positive indicator of economic growth, high levels of unemployment could constrain spending. We’ll be watching to see how quickly those open roles are filled – a mismatch between employer requirements and the skills of the workforce is a downside risk that can take several years to resolve.

Manufacturing recovers but not yet ‘back to normal’

The US purchasing manager’s index (PMI), a measure of the health of the manufacturing industry, and industrial production levels have both recovered well from vertiginous falls in 2020. But production levels have not yet returned to 2019 levels.

Housing stock shortage looms

The housing market came roaring back in late summer 2020 after a brief period of stagnation when Covid-19 lockdowns were at their peak. If you’ve been following the volatile lumber market in 2021, you’ll be familiar with the way in which the housing market has driven growth this year.

In 2022, supply of housing stock rather than demand is the area of concern. Low housing stock levels threaten to push home prices higher, which will slow home sales, in turn shrinking demand for housing-related products and services.

Europe economic outlook 2022: recovery loses steam

Europe’s economy continues to struggle. We forecast growth of just 3.1% through to the end of 2021. In 2022, we expect to see a growth rate closer to 4.8%, lagging behind the US.

In the euro area, 2.3% of jobs are vacant. It has only reached that height once before – in 2019 – in the past eight years. Just like the US, the degree to which skills in the workforce match the skills in demand will determine how long high rates of underemployment persist.

Consumer and business confidence levels have had a bumpy ride, following the ups and downs of the Covid-19 pandemic. Right now, growth is on a downward trend. Overall, the recovery isn’t going as well as it should be. Europe’s post-Covid momentum is fading fast, which is bad news for the US because of the close relationship between the two trading blocs.

China economic outlook 2022: China has an outsized role to play

China is the big question mark looming over 2022. We still forecast 8.5% growth for this year and 5.6% for next year. This is on the optimistic side; signs indicate that the pace of growth could slow rapidly in 2023. Falling retail sales of consumer goods suggests hard times to come.

China represents roughly 20% of the global economy in 2021 but more than 30% of total global economic growth – in other words, it’s picking up the slack from Europe and other slow-recovery regions. If Chinese growth slows, global growth will follow. All eyes are on China in 2022.

Latin America economic outlook 2022: struggling to recover from a lost decade of economic progress

After a decade of GDP stagnation, growth is looking up through the end of 2021 but is set to slow again in 2022. In Latin America, higher public spending in 2020 due to Covid-19 and higher global commodity prices in 2021 are driving up prices while unemployment levels remain high and purchasing power stagnates. With that, unfortunately, the risk of underperformance is high.

2022 and beyond – a bumpy road ahead?

In 2022, growth in all four major regions is expected to slow as reality sets in after an initial post-Covid boost. National debt levels are high, supply-side and logistics issues persist in everything from microchips to US housing stock and inflation is rising. In the next few months, we’ll be watching central banks closely to see whether and how they’ll intervene. Of course, we’ll be watching China’s economic indicators most keenly – any deviation from forecast there will have a ripple effect through the entire global economy.

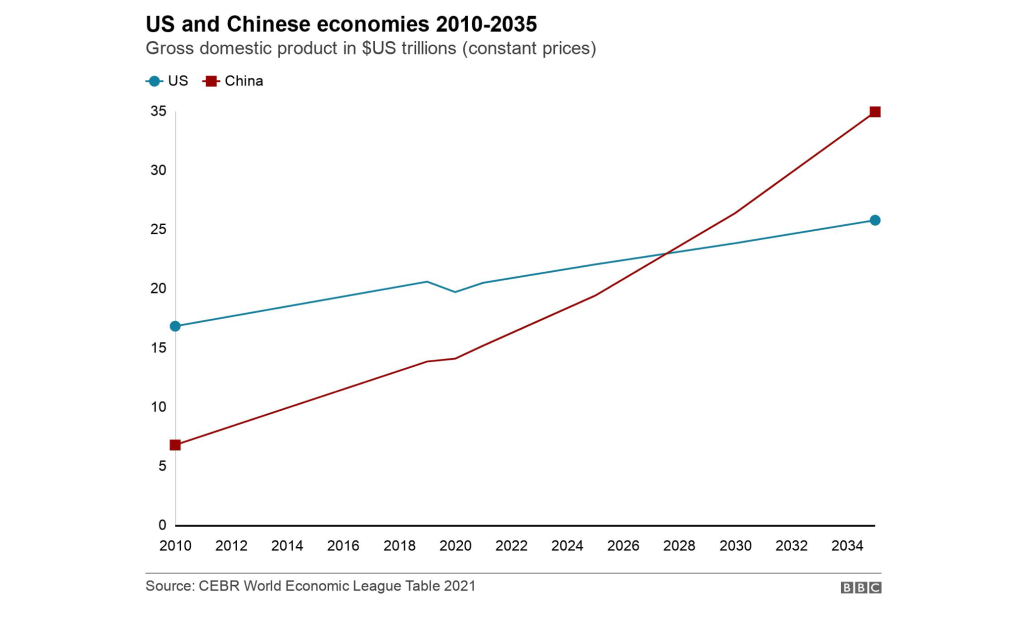

BBC: China will overtake the US to become the world’s largest economy by 2028, five years earlier than previously forecast, a report says.

The UK-based Centre for Economics and Business Research (CEBR) said China’s “skilful” management of Covid-19 would boost its relative growth compared to the US and Europe in coming years. Meanwhile India is tipped to become the third largest economy by 2030.

Although China was the first country hit by Covid-19, it controlled the disease through swift and extremely strict action, meaning it did not need to repeat economically paralysing lockdowns as European countries have done.

As a result, unlike other major economies, it has avoided an economic recession in 2020 and is in fact estimated to see growth of 2% this year.

The US economy, by contrast, has been hit hard by the world’s worst coronavirus epidemic in terms of sheer numbers. More than 330,000 people have died in the US and there have been some 18.5 million confirmed cases.

The economic damage has been cushioned by monetary policy and a huge fiscal stimulus, but political disagreements over a new stimulus package could leave around 14 million Americans without unemployment benefit payments in the new year.

- The Up-skilling Framework for Industrial Leaders

Burgos, August 3, 2026. Overcoming this friction requires a structured, empathetic approach that respects legacy expertise while establishing non-negotiable paths toward digital fluency. The following four-stage framework aligns technological integration with professional respect: 1. The “Expert-First” Software Selection Before purchasing or building a new digital tool, bring your legacy operators into the vendor evaluation phase. If… Read more: The Up-skilling Framework for Industrial Leaders

Burgos, August 3, 2026. Overcoming this friction requires a structured, empathetic approach that respects legacy expertise while establishing non-negotiable paths toward digital fluency. The following four-stage framework aligns technological integration with professional respect: 1. The “Expert-First” Software Selection Before purchasing or building a new digital tool, bring your legacy operators into the vendor evaluation phase. If… Read more: The Up-skilling Framework for Industrial Leaders - The “Stay Interview” Framework for Industrial & Site Leaders

Burgos, July 7, 2026. In the capital-intensive sectors of construction, heavy machinery, and industrial operations, talent scarcity has reached a critical tipping point. For a Managing Director, the traditional reliance on annual performance reviews and retroactive exit interviews is no longer a viable retention strategy. When a senior civil engineer, an experienced site manager, or a… Read more: The “Stay Interview” Framework for Industrial & Site Leaders

Burgos, July 7, 2026. In the capital-intensive sectors of construction, heavy machinery, and industrial operations, talent scarcity has reached a critical tipping point. For a Managing Director, the traditional reliance on annual performance reviews and retroactive exit interviews is no longer a viable retention strategy. When a senior civil engineer, an experienced site manager, or a… Read more: The “Stay Interview” Framework for Industrial & Site Leaders - The Death of the Job Description: Navigating the Human-AI Hybrid Workforce

Burgos, June 8, 2026.- The traditional job description, a static relic of the industrial age, has officially met its demise in the face of the 2026 labor economy. For decades, we hired individuals to fill rigid “roles”—Project Manager, Site Engineer, Estimator—assuming that a single human could or should encompass every competency required by that title. However,… Read more: The Death of the Job Description: Navigating the Human-AI Hybrid Workforce

Burgos, June 8, 2026.- The traditional job description, a static relic of the industrial age, has officially met its demise in the face of the 2026 labor economy. For decades, we hired individuals to fill rigid “roles”—Project Manager, Site Engineer, Estimator—assuming that a single human could or should encompass every competency required by that title. However,… Read more: The Death of the Job Description: Navigating the Human-AI Hybrid Workforce - The era of “AI experimentation” has reached its inevitable conclusión

Burgos, May 7, 2026.- Throughout 2025, most Managing Directors in the construction and industrial sectors treated Artificial Intelligence as a peripheral add-on—a series of pilot programs designed to test the waters of predictive maintenance or generative design. However, as we move through 2026, the industry has hit a critical inflection point. The transition from isolated digital… Read more: The era of “AI experimentation” has reached its inevitable conclusión

Burgos, May 7, 2026.- Throughout 2025, most Managing Directors in the construction and industrial sectors treated Artificial Intelligence as a peripheral add-on—a series of pilot programs designed to test the waters of predictive maintenance or generative design. However, as we move through 2026, the industry has hit a critical inflection point. The transition from isolated digital… Read more: The era of “AI experimentation” has reached its inevitable conclusión - Technical Talent Management in the Digital Age

Burgos, April 8, 2026.- The evolution of the technical workshop in the green industry has undergone a silent but radical metamorphosis, moving from the rhythmic clanking of wrenches to the silent processing of diagnostic software. As a Managing Director with an engineering background, I observe this shift not just as a change in tooling, but as… Read more: Technical Talent Management in the Digital Age

Burgos, April 8, 2026.- The evolution of the technical workshop in the green industry has undergone a silent but radical metamorphosis, moving from the rhythmic clanking of wrenches to the silent processing of diagnostic software. As a Managing Director with an engineering background, I observe this shift not just as a change in tooling, but as… Read more: Technical Talent Management in the Digital Age

Leave a comment